Community Takes All: The Power of Social+

There’s one rule of thumb that’s proven true over and over again: the best version of every consumer product is the one that’s intrinsically social.

Tiktok. Fortnite. Minecraft. Pinduoduo. These phenomena are what I call “social+” companies: companies that take a single category—from gaming to music to ecommerce—and build an integrated social experience around it.

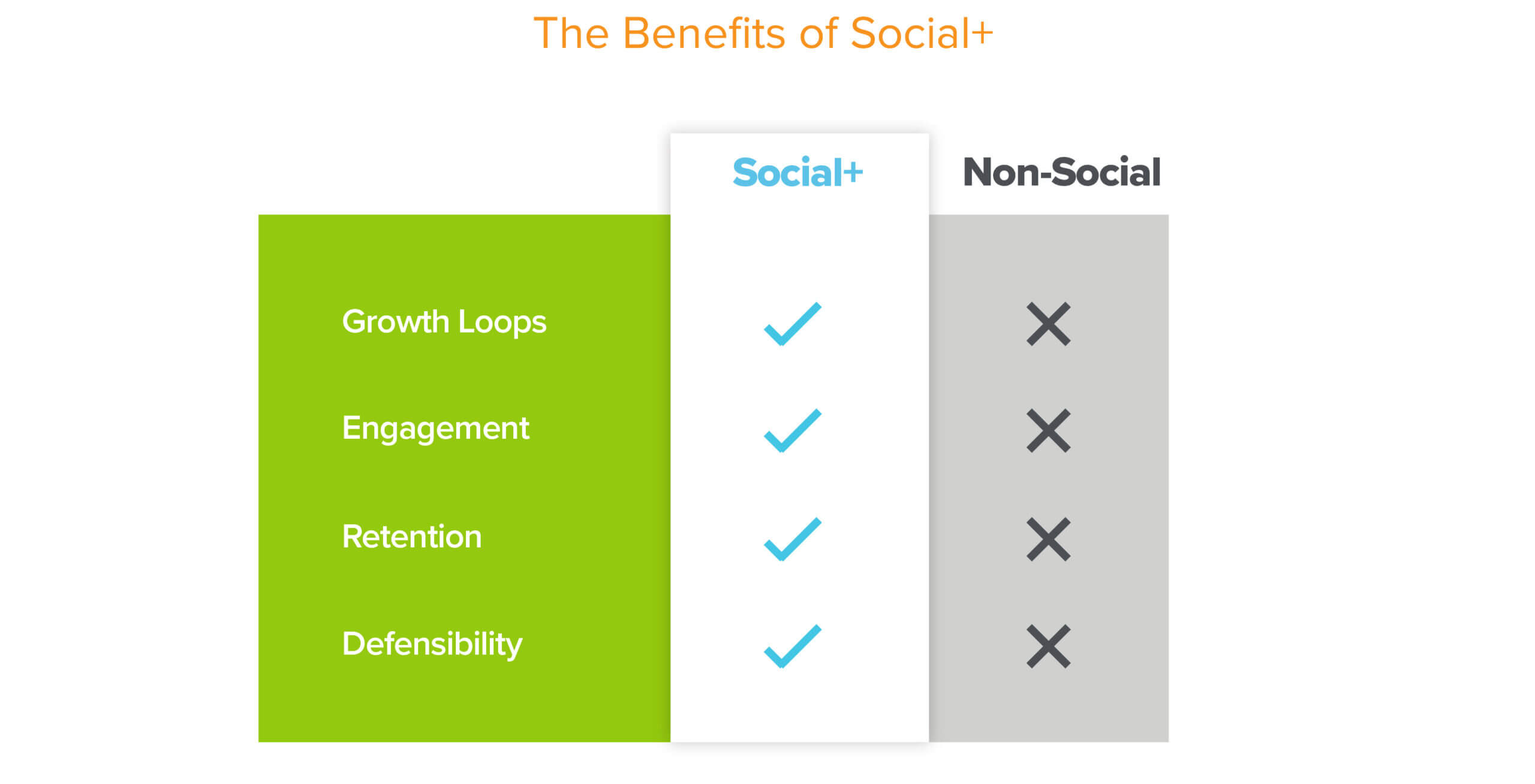

Any product that has a social component baked in has fundamental and asymmetric advantages over competing non-social products in that category: better growth loops, better engagement, better retention, better defensibility. And because social+ companies are network and community driven, that advantage accumulates over time.

The key isn’t the rule itself, but the implication for founders trying to compete: No category is really won until the social product is built. Even seemingly entrenched incumbents in big, enticing categories like personal finance and real estate are surprisingly vulnerable to scrappy upstarts if they’ve failed to make their products sufficiently social.

Herein lies the opportunity. Not every product category has had its social moment—yet. Just as every industry makes the crucial transition from analog to digital, nearly every category of company will eventually make the fateful transition from single-player to multiplayer, from company-driven to community-driven, from individual to social.

Through the inevitable cycles of consumer social, there is enormous opportunity for founders who can thoughtfully build social+ companies.

The hallmarks of a social+ company

A social+ company combines the community and network of a social product with a specific category, form factor, or experience. This can range from fitness (category) to audio (format) to games (experience), but the defining factor is that these companies are social at their core.

Usually, that means three conditions are met:

1. Social+ companies have a unique and proprietary social graph that is purpose-built for that product.

Having a social graph is table stakes; the true test is whether the graph is unique and inseparable from the product. For a social+ product to break out, it needs to reach a group of people that would only be bought together by that specific product experience. Building a product on top of iMessage or Facebook or Snap’s social graphs can be great, but the network belongs to them, not you. At the end of the day, those platforms can allow any other company to build the same product as yours on that graph (or, worse yet, auction off the right to access it). But if a social graph is purpose-built for your product or experience, then you’re building something special and defensible. Comparing the strength of the Fortnite community of today to the social games that were built on Facebook in the aughts supports this theory. It doesn’t mean you can’t bootstrap off another network, but ultimately you need to own your community.

2. The social graph is critical to the product.

The social element needs to be integral to the experience, not an afterthought. We’ve all used clunky and poorly designed products that take a fun single-player experience and thoughtlessly try to layer on a social dimension. Designing an annoying “invite a friend” pop-up where it’s not wanted or needed is not a social+ product. To be a social+ product, the social element needs to be critical to the overall product experience. Many media platforms let readers share stories with a select group of friends; this is different from social media sites like Twitter where the social graph is the only thing producing and curating content. In the former, the graph isn’t critical to the product; for the latter, it is.

3. Peer-to-peer social engagement is baked into the product itself.

Just as it’s easy to mistake a media product for a social product, it’s easy to confuse an audience with a community. An audience passively consumes, while a community engages with each other. Social+ products feature authentic engagement between the users in the network, not just with a single curator or creator. In the fitness world, Strava creates true peer-to-peer engagement, while a company like Peloton is largely focused on engagement with instructors. Both are social to a certain extent, but only when a company demonstrates that authentic engagement between users will it reap the advantages of being social+.

The challenge in building a social+ company

Frankly, one of the reasons social+ companies present a unique opportunity is that they’re hard to build—both from both a product design and a distribution standpoint. Really hard. As a founder, I learned these lessons the hard way. I wasn’t alone: even very successful companies fail at orchestrating a social dynamic that feels authentic, rather than awkward. Remember fist-bumping your rideshare driver back in the day? Or rolling your eyes when a bank or a direct-to-consumer T-shirt company refers to you as “family”?

There are a lot of ways to go wrong building social+.

A social+ product typically has both an interaction layer and a transaction layer. The interaction layer appeals to a user’s emotional and cognitive side, while the transaction layer is more functional and rational. From a product and marketing perspective, combining those two distinct tasks into a coherent experience can be a delicate balancing act. But when the emotional layer and the transactional one are well-designed and mutually reinforcing, that’s when the magic happens.

The best examples work like the Chinese group shopping app Pinduoduo. The transactional act of purchasing (cheap prices!) is inextricably linked to the social and interactive dimension (cheap prices because of friends!!). More friends, cheaper prices! Neither layer feels inappropriate, and each layer feeds off the other other in a seamless way. That is social+ product design at its best.

This balancing act applies not just to product design, but to your distribution, business model, and even what categories you operate in.

How to build social+

Well-designed social+ companies address four key areas:

It’s important to understand that “social+” isn’t merely a framework or a marketing ploy. Social+ companies can start with a familiar single-player concept, but it’s thoughtful design and that deliberate social/transactional balance that distinguish them from the rest.

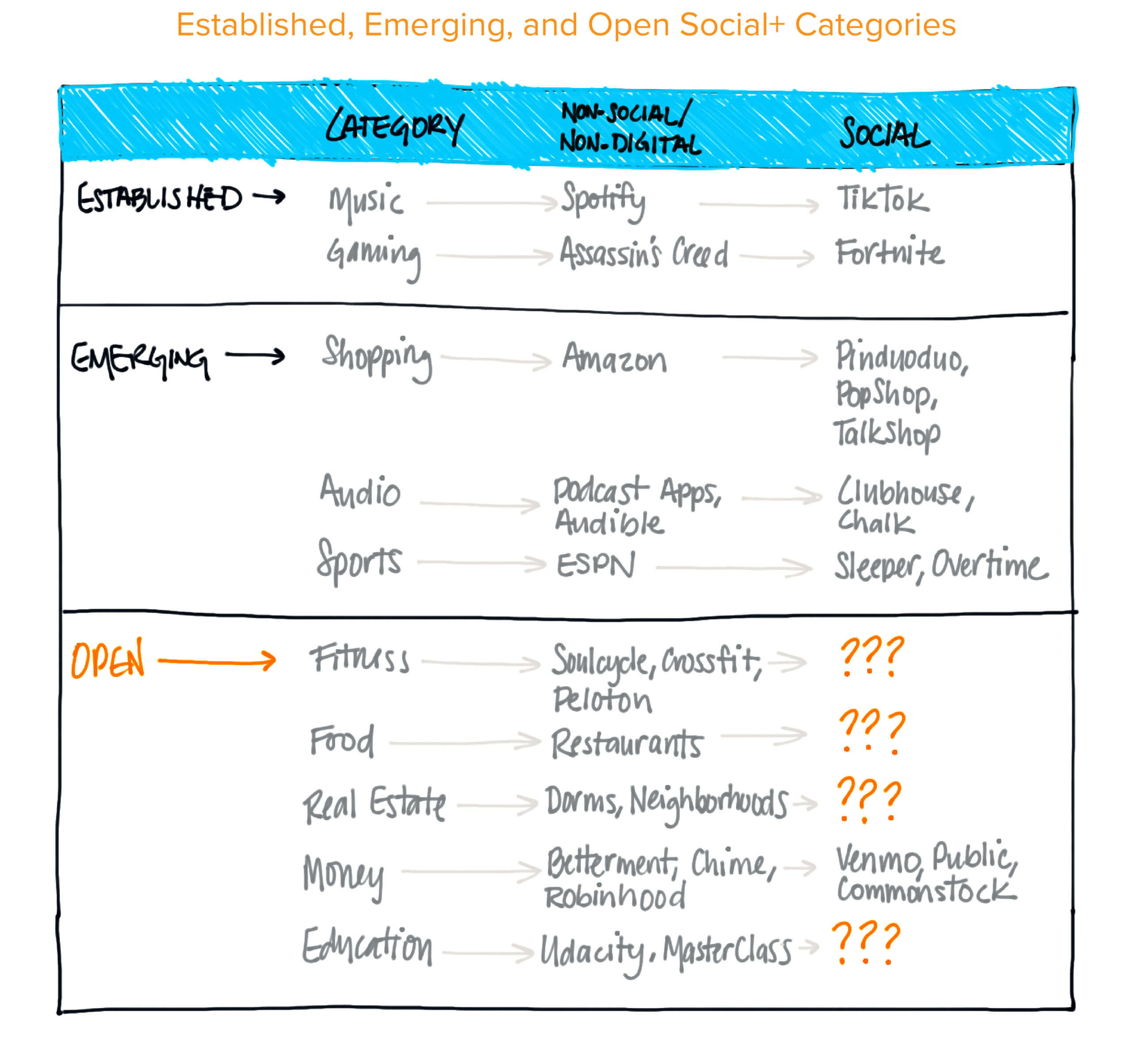

Categories that have gone social+

1. Social+ Music: Spotify vs. Tiktok

Spotify is great, but it’s primarily a single-player experience. Music, on the other hand, is an inherently social experience. Tiktok—originally, musical.ly—figured out how to make music social by licensing music, introducing viral “challenges,” and making user-generated content easier to create, even if they didn’t technically build a social graph. After 14 years, Spotify’s market cap is approximately $50 billion. Though Tiktok is still private, recent public estimates suggest it is well on its way to surpassing that benchmark in less than 5 years.

2. Social+ Gaming: Assassin’s Creed vs. Fortnite

Assassin’s Creed may be one of the most successful game franchises ever, but it lacks the social elements of Fortnite or Minecraft. There is no user-generated content and no real social graph within the game. The Assassin’s Creed franchise is estimated to be worth $300 million, while Fortnite was estimated to bring in nearly $2 billion last year alone. This is why the best games are more like social networks than Hollywood hits.

Emerging social+ categories

1. Social+ Shopping: Amazon vs. Pinduoduo

It may seem odd to call social commerce (or a $100 billion company) “emerging,” but in the West, at least, we believe commerce is still in the process of tipping into the social realm. In its analog form, shopping can be extremely social. While we don’t expect Pinduoduo—or any other social shopping product—to overtake Amazon any time soon, the fact that Pinduoduo has gone from a market cap of zero to more than $100 billion in less than five years shows the potential of social commerce.

2. Social+ Spoken Audio: Audiobooks/podcasts vs. Clubhouse/Chalk

Podcasts, audiobooks, and the entire audio format are having a unique moment. But while the medium in the explosive podcast era has largely been single-player and passive, that is starting to change. Clubhouse and a handful of other startups have taken the same form factor, but layered in a social network and more user-generated content. Though it is still early days, social audio is clearly an emerging category.

3. Social+ Sports: ESPN vs. Sleeper/Overtime

Sports are inherently social. We watch games together, fandom is passed down from one generation to the next, and it’s not quite the same on your own. ESPN and the leagues provide the media and the content, but companies like Sleeper and Overtime are building true social+ experiences around sports.

Open social+ categories

Interestingly (and encouragingly), there are tons of categories that are still open for enterprising founders. Some are naturally more social than others, but we believe that eventually *every* category will go social. The most interesting thing about the social+ wave isn’t the categories that have already gone social, but how much opportunity still exists. There are many activities in which the analog version is inherently social, but the digital version is still a single-player experience.

1. Social+ Fitness

For many, working out is an inherently social experience. For a growing segment of super-users, Crossfit and SoulCycle are more like cults than products. But so many fitness-related digital products are solo experiences that fail to capture the community of their analog equivalents. Strava, for example, has some magical social elements, but hasn’t completely cracked the code yet. Peloton’s leaderboard is fun, but it’s a toe-in-the-water of what could be a deeper social experience. There’s so much more to build here that could capture the community of fitness enthusiasts. Imagine how engaging the first truly global social+ fitness product will be.

2. Social+ Food

Eating isn’t always social (especially in COVID times), but when it is, it’s very social. Restaurants and dinner parties are amazing, but it will be a while before we go back to those in full force. From virtual kitchens to food delivery to meal kits to plant-based food, we’ve seen a lot of innovation in food of late, but so far social+ food has proven elusive. We believe companies like Snackpass and Ritual show promise, but there is still plenty of room for innovation.

3. Social+ Real estate

Where and how we live is also a social experience. Whether roommates, neighbors, or local communities, a lot of people choose where to live and work based on their social experience. Real estate is a trillion-dollar market; enormous companies such as Zillow and Opendoor have been built in the space. Whoever can thread the needle—layering the social experience of our neighborhoods and communities on top of the transactional layer of real estate—will have something magical.

4. Social+ Money

Social + money is a holy grail. I spent years trying to crack it at Frank. While the challenges of building in social+ are clear, so is the vastness of the opportunity. Venmo’s public feed and WallStreetBets on Reddit are the tip of the iceberg. More recently, we’re seeing tons of experiments, ranging from Public to personal tokens. I don’t know exactly what will work, but I’m convinced that eventually, something will. Every good idea has its moment.

5. Social+ Education

For many, school is a core pillar of their social network. Yet most of what we’ve seen thus far in online education is passive and single-player. This, too, is changing, both in the U.S., and internationally. Remote education companies like Outschool are starting to layer in more social features to improve both the experience and efficacy of their programs.

The future is social+

“Social” as a product category has had a rough go of it recently. Many associate the term with misinformation, outrage-driven algorithms, clickbait-driven business models, and the challenges of the attention economy. But at our core, humans are social beings. We crave connection and community—beyond social media—and things start to fall apart when we don’t have it.

“Social” is a universal and timeless need.

That’s why, despite all the challenges, we continue to look for the best ways to connect with each other in interesting, engaging, and delightful ways. It’s why, despite the potential pitfalls, founders and product builders continue to build experiences that foster strong community. It’s why, even in the face of pessimism, the world of consumer social is back, continuing its winding march towards the perfect product and experience.

“Social” doesn’t exist in a vacuum—it’s frequently layered on top of an activity or experience. And this is why the concept of social+ is so important. It can help us find ways to layer social into so many other activities that we already know and love. It can help us find community in everything from video games to music to workouts. Social+ occurs when delight-sparking utility is thoughtfully integrated with that essential human connection. That’s powerful because, ultimately, the more ways we find to connect with each other in authentic and positive ways, the better.

Social Strikes Back is a series exploring the next generation of social networks and how they’re shaping the future of consumer tech. See more at a16z.com/social-strikes-back.